18860 Nordhoff St #204

Northridge, CA 91324

My Blog

Q2: 2024- Los Angeles Housing Market Update

Posted On: April 20th, 2024 4:55AM

Can you believe we are in mid April & in Q2 of the year? Unbelievable!

In my real estate world the market has been keeping us on our toes and we are noticing a definitive difference between starter homes and the rest of the LA housing market. Allow me to share more.

As you know affordability has gone through the roof and the ones that are getting squeezed are first-time home buyers. Higher property values, with higher mortgage rates and fewer homes coming on the market in the entry-level price ranges is making things harder for the prime first-time home buyer, which are millennials. But there is more. Buyers may now run into an additional fee which is their real estate agent’s representative compensation.

I recently handed over keys to two different young couples; one couple had the sweetest 2 year old boy and the other couple was expecting their first child. These are the every day buyers that we are assist today. Millennials have been getting married and having babies and now want to own a home.

Unfortunately, with higher mortgage rates and higher home prices, many have been unable to purchase. Majority of last year and pretty much all this year, interest rates have been vulnerable and spiking up similarly like gas prices. For nearly two years buyers have been sitting on the sidelines, waiting for either home values to plunge or mortgage rates to drop. Yet, neither has occurred.

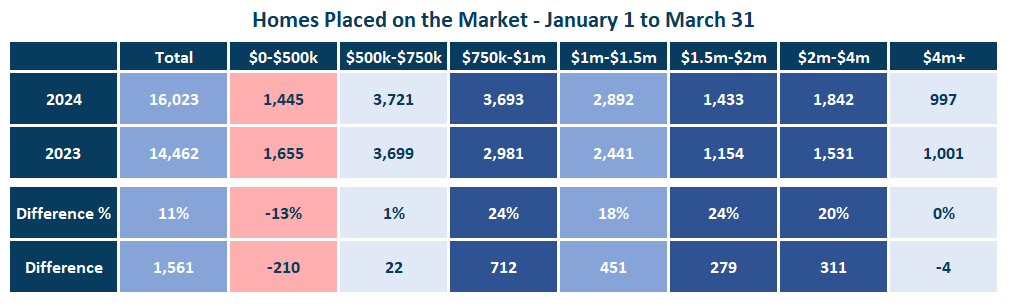

Taking a deeper look though, within the last few months prices above $750,000 have had a lot more activity than last year. See the chart below.

The data above illustrates the differences between starter homes and the rest of the market.

In 2024, through March, an extra 1,561 homes were placed on the market, 11% more compared to 2023. Yet, there were 4% fewer FOR-SALE signs for properties below $750,000. On the other hand, for properties above $750,000 an extra 1,749 (which is 19% more) of new listings were placed on the market. This is affecting the entry-level market which is suffering from a chronically low supply. As a result of the limited inventory of starter homes, the Expected Market Time for properties under $750k, which is the number of days from when the property goes live to when it closes, is 48 days. To paint a better picture of this, typically upon an accepted offer, the escrow time period is 30 days, which means homes under $750k are only lasting about 18 days active on the market before going pending.

For current homeowners, well they are “hunkering down” in their homes and are unwilling to move due to their current underlying, locked-in, low fixed-rate mortgage. Through March, 28% fewer homes are on the market compared to the 3-year average before COVID (2017 to 2019). Starter homeowners are even more inclined to stay put compared to homeowners in the higher price ranges. Many cannot afford to sell their homes and trade their low rates for today’s 7.4% mortgage rate. It simply does not make economic sense. According to the Federal Housing Finance Agency’s National Mortgage Database, 84% of Californians with a mortgage have a 5% or lower rate, 67% are at 4% or lower, and 30% are at 3% or lower.

With the recent Consumer Price Index (CPI) inflation report and other hotter-than-expected economic reports, this week rates spiked more than a quarter percent to 7.44% as of April 15th. We also saw a spike in active listing inventory which increased by 610 homes in the past two weeks, which is up by 8% in new listings. This is not unusual as demand typically downshifts a when rates rise, allowing the inventory to climb so we foresee inventory continuing to climb up if rates remain above 7%. We’ll see how that plays out as we move forward into quarter 2.

Like always, please know I am here to be of guidance with all of your real estate needs. If you know of someone who is thinking of buying or selling please forward this market update to them. It is truly an honor to be of service to you and your loved ones.

If you have any questions please call or text me anytime. My cell phone number (510)927-6588. One last note, if you need any plumbers, roofers, electricians, or are looking into estate planning, trust or wills, and/or investment opportunities I have amazing connections with other great professionals and would like to share my referrals with you.

Whatever it is I can do to help, I am here for you.

Wishing you a lovely rest of the week.

With Care,

DTI: Important for when buying a home

Posted On: April 20th, 2024 4:51AM

Any time you have more income and less debt, you’re in good shape in life. That said, there is an ideal ratio between your debt and income in order to qualify for a good mortgage.

When your debt to income ratio is on the high side, you run the risk of not getting a good loan (or not getting a loan at all) if your income were to take a hit right before or during the loan funding process.

Conversely, having no debt can work against you, too, as your credit score might not be as robust as it needs to be if you have a seasoned credit record showing you accruing some debt and then paying it off.

Here's a closer look at what your debt-to-income ratio is and how it works.

Your Debt-to-Income Ratio Explained

It’s fairly simple. You have income that comes in from your job, investments and other sources from which you get paid. This is the money you use to service the debt.

Then, you have your debt: recurring and regular spending. Every month, you have recurring bills like cell phone, car, cable, mortgage, credit cards, etc. After that, there’s regular spending on things like food, gas, clothing, etc.

Now, if more of your income goes to paying your debts instead of being put away for savings, then you might have a high debt-to-income ratio (DTI) scenario. Specifically, the debt-to-income ratio is a number that details the relationship between your total monthly debt and your gross monthly income.

If we were to put it into a formula, it would look like this:

DTI = total monthly debt payments/gross monthly income

Here’s an example: Say you pay $1,500 a month on your mortgage. You pay $500 a month for your automobile loan and other than that, have no other substantive debt. Your total monthly debt payments come to $2,000. At the same time, let’s assume your gross monthly income - the money you earn before taxes and any deductions you take is $6,000.

Total monthly debt payments ($2,000)/Gross monthly income ($6,000) = DTI 33%.

It’s that simple. Now, let’s take a look at why your lender puts so much importance in your DTI.

Why is your DTI so important?

Your DTI tells you a lot about you and how solid - or problematic - your financial situation is.

For instance, if your debt needs to be covered by 60% of your income, any negative change to your income will leave you in a tough spot. Or, if you have to increase your spending for other areas of your life, let’s say doctor’s visits and medical expenses, you could have a rough go of it in keeping up with your debt payments vs. someone who has a DTI, half that, of 30%.

Essentially, the lender looks at your DTI as a key indicator of risk in doing business with you. Home buyers with higher debt-to-income ratios are more likely to default on their mortgages and other debt in general.

This is why calculating your DTI will be part of the mortgage underwriting process. In general, 43% is a high DTI, but there are programs that can have a DTI of up to 50% and still get what lenders call a qualified mortgage.

Overall, a good DTI means you are more financially secure. The lower it is, the more affordable your debts are. With a low DTI, you can handle fluctuations in your income better and you’re a better risk for people who want to invest in you. If you’d like someone to take a look at your DTI and let you know what kind of shape you’re in to get a great mortgage, click here. You’ll get access to a no-cost consultation with a credible financial expert who can give you the guidance you need to get your DTI where it needs to be to get some great deals on a mortgage.

To connect with a great lender please let me know. Depending on your current financial circumstances I will redirect you to the best lender according to your particular scenario. Call or text me anytime. I am here to be of guidance and service from beginning to end of your home buying venture~!

Dear HomeOwner and Future buyers

Posted On: February 21st, 2024 3:43AM

Happy February, Friends!

I wanted to share this information regarding the Homeowners’ Property Tax Exemption in case you are a homeowner or know of anyone who currently owns a home.

This is a one time application and the “homeowners exemption” will be applied automatically to your tax assessment until you move out or sell. The claim may be filed any time after you become eligible, but no later than February 15 to receive the full $7,000 exemption for the next fiscal year, which begins July 1. Attached is the The State Board of Equalization Taxpayers’ Rights Advocate Office Information Sheet for additional information and steps on how to apply. Here is the link as well: Information Sheet

For those who currently do not own a home and have not been homeowners in the past 3 years: The Dream for All Appreciation Program is coming back possibly early Spring.

The Dream For All is a conventional loan goverment assistance program that grants the buyer up to 20% of the buyers down payment or Up to $150,000 whichever is less; and if and when the buyer decides to sell or refinance the property the borrow would need to pay back the original amount that the program covered plus an additional 20% of the total equity earned. So initially the program can grant 20% down payment upfront and if and when you sell you or refinance the property you'd have to pay back what was borrowed and an additional 20% of the equity. In my opinion, thats not bad if you are looking to stay at that property for at least a decade. There are some requirements so if this is something of interest just let me know.

I am always here to update you with the market update and when needed I am just a phone call away.

2024:Q1- Market Update & Forecast

Posted On: February 21st, 2024 3:41AM

As the dawn of a new year unfolds, I wanted to take this opportunity to wish you a fantastic start to 2024! I hope this year brings you renewed energy, priceless memories, and maybe even a new home?

In the ever-evolving realm of real estate, understanding market trends and forecasts is crucial for making informed decisions; and that is what I am here for. To keep you updated and well-informed so I'm excited to share valuable insights and predictions that could significantly impact your real estate ventures this 2024.

First, let us look back at what happened in 2023 in terms of inventory, demand, and the Expected Market Time. Last year the Los Angeles inventory started with 7,664 active listings, the second lowest level to start a year since tracking began in 2012, only behind 2022’s 4,432 anemic start. Prior to the pandemic the average start was 10,079 listings. Inventory only dropped the first two quarters reaching 6,778 listings! That's extremely low, especially as we cruised throughout the summer season. With rates stubbornly remaining above 7% since July and even reaching 8% in October, the peak was not reached until the start of November where inventory reached 9,053 homes, growing by 34% since April. Then rates declined, and so did inventory and we finish up the year with just under 7,000 active listings, lower in count from when we started the year in January 2023.

Although the interest spike highly impacted affordability, if a property was priced correctly, the results of the low inventory still caused the housing market to be more of a sellers' market. It was not as crazy as the past few years where we saw 10-20 offers on the table but buyers were still competing against a handful of other buyers. We didn't see much of the crazy seller's request on counter offers but we did see majority of counter offers with request of shorter contingencies and “sold as is” terms. Typically, buyers who were looking at homes under $1.4mil had to still process a few offers before getting an offer accepted.

So we ask ourselves what has caused the low inventory? Well homeowners opted to stay put and “hunker down,” enjoying their fixed, low monthly mortgage payments that they locked in during the record low interest rates during the covid season. A remarkable 85% of California homeowners with a loan enjoy a fixed rate at or below 5%, 68% of those homeowners are at or below 4%, and 30% locked in a rate at or below 3%! With property values increasing and interest rates doing the same, homeowners who considered selling would start running numbers with their loan consultant and things just didn't make sense! Most likely that seller would pay twice to three times more than their current mortgage payment for a smaller home! I am speaking from firsthand experience as well!

So, what can we expect for this New Year? Well, if only we could have a crystal ball, right? But looking at data and eating, breathing, and living real estate every day I feel pretty confident that if property values didn't crash in 2023, they for sure won't be crashing this new year. From the experts we are forecasted to see an increase in values at around 4-5%. We forecast to see interest rates floating throughout the year from mid 5% to the high 6%, low 7’s. Inventory may possibly continue to stay tight until we consistently see rates sticking in the low 6% and more movement when rates reach the 5’s.

We also hear rumors of the California Dream for All Shared appreciation program granting 20% down of your down payment coming back in a couple months, so if this was something of interest, I advise that you start your required online class. Additionally, the housing market will follow a typical housing cycle. Spring is the strongest in terms of demand, followed by the Summer Market, then the Autumn Market, and finally the Holiday Market. Luxury housing will be sluggish and will continue to transition to normal, longer market times, often taking months to procure a sale while properties under $1mil will have competition if priced accordingly to the current fair market value.

The bottom line is that this is an election year, and the economy will cool down sometime in 2024. When that occurs, rates will drop, and the housing market will heat up. No matter what, there will be more homeowners opting to sell their homes, pending sales will increase and surpass 2023 levels, and there will be more closed sales. Ultimately, how hot the housing market will get depends upon when the overall economy downshifts but know I will be here to share all those market updates with you. I am only a phone call away for you your friends and your family so if you are thinking of buying, selling or investing just let me know. My cell phone number is 510-927-6588 and you can call or text me anytime. With lots of love and good vibes, I wish you a prosperous New Years! Cheers to the good things that are yet to come~!

—

I would also like to share today’s rates shared by one of my trusted loan consultants:

- Government Loans (FHA / VA) are in the high 5's and low 6's

- Conventional Loans up to $765,550.00 are in the low to mid 6's

- High Balance Loans $765,550.00-$ 1,148,325.00 are in the mid to high 6's

- Jumbo loans above $1,148,325 are in 6's

- Bank statement loans – They are available with 10% down again! 8's and 9's depending on down and credit score.

- No income qualifier - 40% down with reserves! In the 8's!

- 0 down loans are in the high 7's - 660 credit score min right now, up to $740,000.00.

- Private Money lenders – hard Money Loans - 35% down!

Lastly, some food for thought and after looking at today’s rates, if your estimated preapproval interest rate is let's say 5.75%, we can always try to negotiate to buy down a point by the seller, bringing that rate down to 4.75%! Now that’s HOT!

With Care,

Your Realtor

Linda Mendoza

CalDre#02014425

Q3: Los Angeles Market Update

Posted On: September 6th, 2023 11:08PM

Hi friends,

I hope this message finds you and your family well and healthy. I am thankful that the hurriquake did not cause too much damage. I connected with a handful of clients within the last couple of days and no roof leaks nor water intrusion thank God! For my household, we went up on the roof and applied Henry’s roof sealant on some areas to add an extra layer of protection so no roof leaks… however I did have water intrusion on one side of our house. I believe it's due to some minor stucco cracks so this week we’ll be adding some cement to the stucco to prepare for the upcoming rainy months. Although the water intrusion did not do too much damage, it was unexpected. With that said, I am going to freshen up and reread my homeowners policy to review my coverage. Understanding your policy is crucial to avoid any future catastrophe, so homeowners, when you get an opportunity please review yours so you know your coverage incase ever needed!

Anyhow I’ve been wanting to write to you now that kids are back at school and summer is coming to an end. The summer was HOT! And I am not referring to the weather but to the housing market. It seemed like back then during that crazy covid season where things were going as fast as hot cakes! According to Freddie Mac’s Home Price Index, since the COVID shutdown in 2020 to today, the Los Angeles metro has increased in property values nearly 40%!

Multiple offers, no appraisal contingencies, and prices going way above asking was what we saw during COVID. It wasn't until last year late Q4 right around November, December to early Q2, in January, February, where things slowed down. Speculators thought the next housing market crash was finally here. Then March hit. And so did the Dream For all Appreciation program; where it stirred the pot yet again and the market took off once more. Since March and through the 2023 summer we have experienced a very hot sellers market EVEN WITH the vulnerable and soaring interest rates spikes.

Milk, eggs, meat, and all services in general have significantly increased in price and we have seen inflation affecting the housing market as well. Before COVID, 66% of all closed sales in Los Angeles were below $750,000.00. Today in 2023 only 41% of all closed sales are under $750k; that is a quarter difference.

What does this mean? For buyers that are anticipating more coming soon homes in the affordable price ranges it is simply not in the cards. The number of opportunities is diminishing over time. I call this the new cost of living. The point is that more and more homes are surpassing the $750,000.00. Pre COVID season finding a $500,000 single family residence in Los Angeles was doable, today not even a condo! I mean look at rents. According to LivingCost.org, an average cost for a 1 bedroom in the city is $2,239.00, a cheap 1 bedroom apartment outside the city center is running for $1716.00. Talk about a 3 bedroom apartment in the city, the average monthly cost is $3,852.00; outside the city center a 3 bedroom apartment average is $2,934.00. These standards are for apartment averages, not single family homes!

So what's next? Well, remember that California Dream for All Appreciation program that I mentioned earlier and was in such high demand lasting only 11 days before the money was gone back in March? Well, as always, I try to stay in front of all real estate things and rumors are that this program will be available again this upcoming October. All of my lending partners are telling potential buyers to get pre-approved NOW if they want to buy a home using this program so they can complete the required online course sooner than later. This program helps buyers who have not owned nor purchased a home in the last three years with 0% down and no PMI. During the autumn and winter season things usually cool off but this program and the shortage in inventory may keep the market boiling throughout the year.

Before I wrap things up I do want to let you know that if a property is even slightly overpriced due to the high interest rates, and even during this feisty market, surprisingly it may sit on the market and go through a couple price reductions until the price meets fair market value. Yes sellers, even if the property is just slightly overpriced. Right now for buyers, every penny counts so sellers, I am reiterating this, please be careful with over pricing. It can affect your listing a lot if you over-priced the property even if it's by $15k so please listen to your agent and don't be stingy!

With all this said I will continue to keep you updated with all real estate market trends. Know I am always here for you, your friends, and your family. Wishing you a lovely rest of the week.

With Care,

Linda Mendoza